Your borrowing power allows you to use one of the most powerful investment strategies available. The strategy is called leverage, after the principle of using a small force to create a much larger force. Leverage is one of the governing principles of growing a real estate portfolio.

Here's how it works. Let's say that as a homeowner, you are able to borrow $100,000. If you use the $100,000 as a down payment, you could finance a property worth $400,000. Suppose that over the course of a year, the property you acquire appreciates by 15% to $460,000. This means that your $100,000 investment would have netted you a profit of $60,000 in one year, a return of 60%.

Few investments can get you this kind of bang for your buck and it is this principle that has built many real estate empires. Leverage, however, has big downsides as well as upsides, so you should know your market well before taking action.

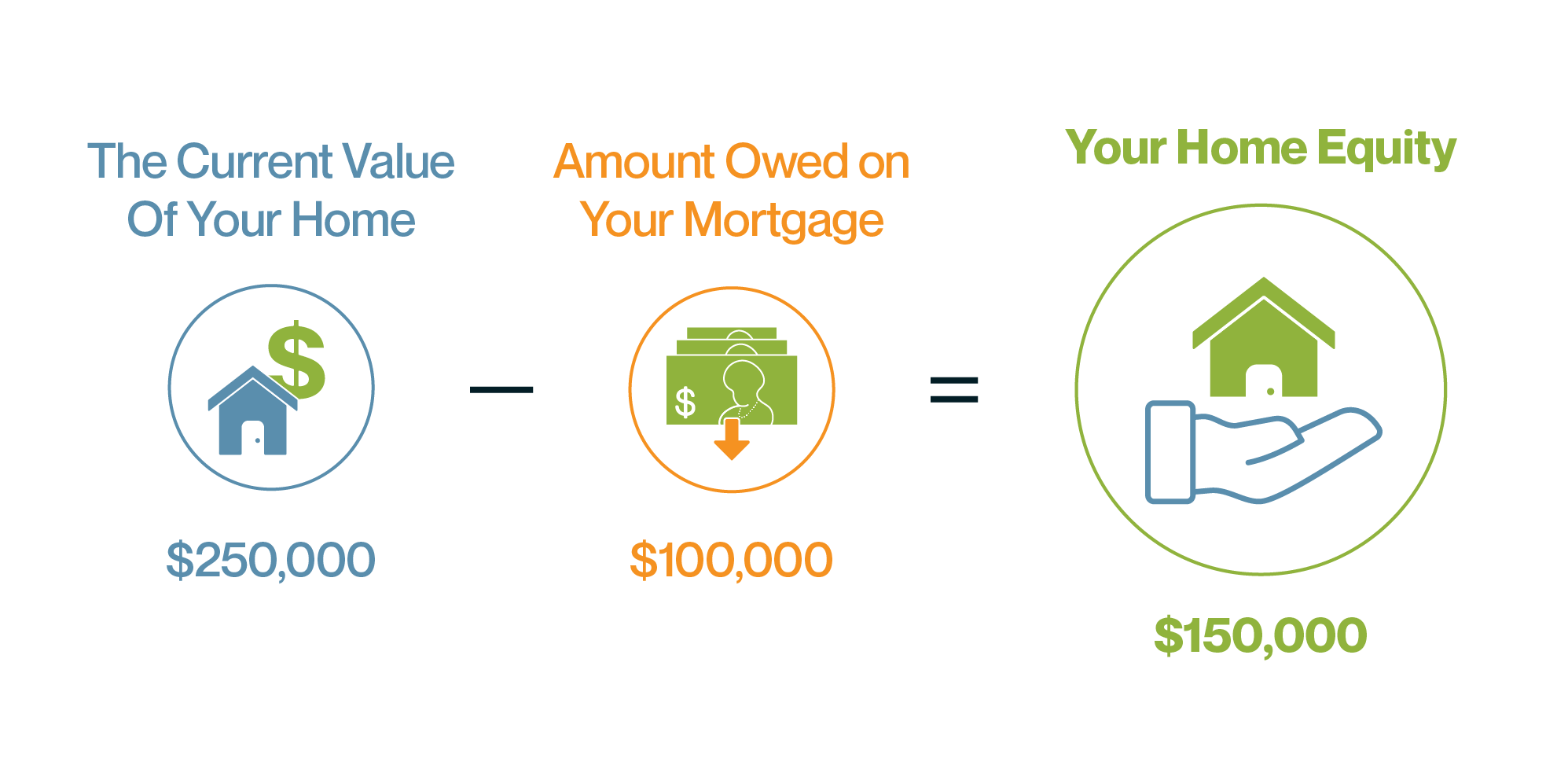

The equity in your home and your ability to pay off a mortgage will determine the amount you can borrow to expand your real estate portfolio. A conservative approach is to allow for a 25% down payment. Therefore, if your lend-able equity qualifies you for a loan of $75,000, you could use that as a down payment for a property worth $300,000. Or, you could finance a $75,000 renovation.